Context reporting in FIA

Attribution reports can be hard to interpret. Typically, working out why and where a portfolio made its returns requires you to know how the market moved, how the portfolio was positioned against its benchmark, and what risks were in play –

and how these factors all fit together.

A conventional attribution system will take you most of the way there to understanding the above, but usually there is a fair amount of time-consuming cross-refencing required to gain a full understanding of where the portfolio manager’s strategy worked, and where it didn’t. This is why we’ve developed the context report as part of our attribution reporting suite.

The context report

The context report is based on the numbers shown in our standard interactive report but goes considerably further to assist you in interpreting the results. The report

- isolates the top and bottom sources of contribution in your analysis. If you have a portfolio and a benchmark, the report can also include top and bottom active returns. These sources can arise at the portfolio, the sector or the individual security level.

- displays the contribution to return of each source, together with the associated portfolio positions, the risks, and the market movements that led to that contribution, and the mathematical relationship showing how they are related.

Bottom-up context reporting

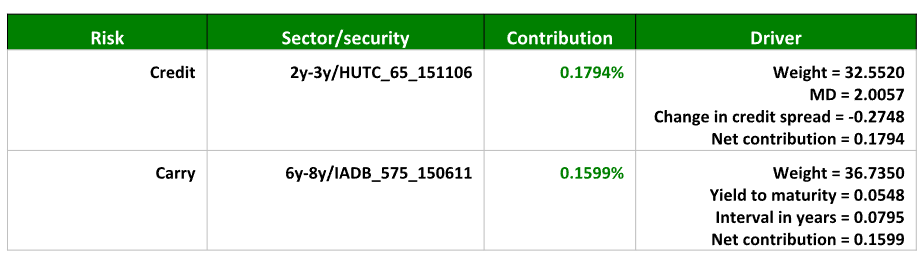

For instance, suppose the context report highlights the following two factors as the highest contributors to return in a portfolio. The context report will appear as follows:

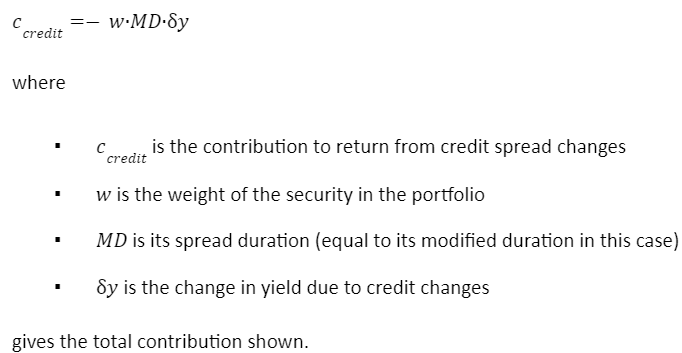

The highest contributing security or sector in the portfolio was due to the HUTC 6.5% bond, which generated 18 basis points of return due to changes in credit spreads. The report shows that its weight in the portfolio was 32%, its modified duration just over two years, and its credit spread fell by 27 basis points over the calculation interval. Combining these together using the expression

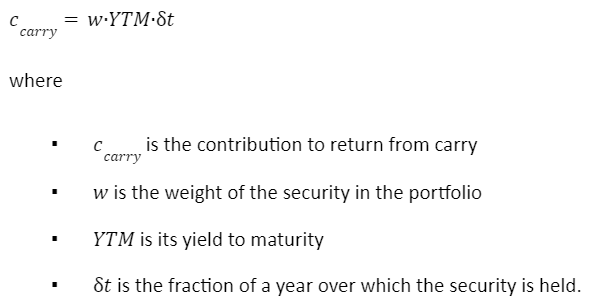

The second highest source of return was due to the IADB 5.75% bond, which generated 16 basis points or return due to carry. The report shows that the bond’s weight in the portfolio was 37%, its yield to maturity was 5.48%, and the elapsed time was 0.0795 of a year. Here we use the expression for carry contribution

These numbers will allow you to quickly gain an appreciation of the main drivers of your portfolio, and why they occurred, by providing all the relevant data in one place. The information is available elsewhere in FIA’s reports, but the context report presents it all in one place.

Top-down context reporting

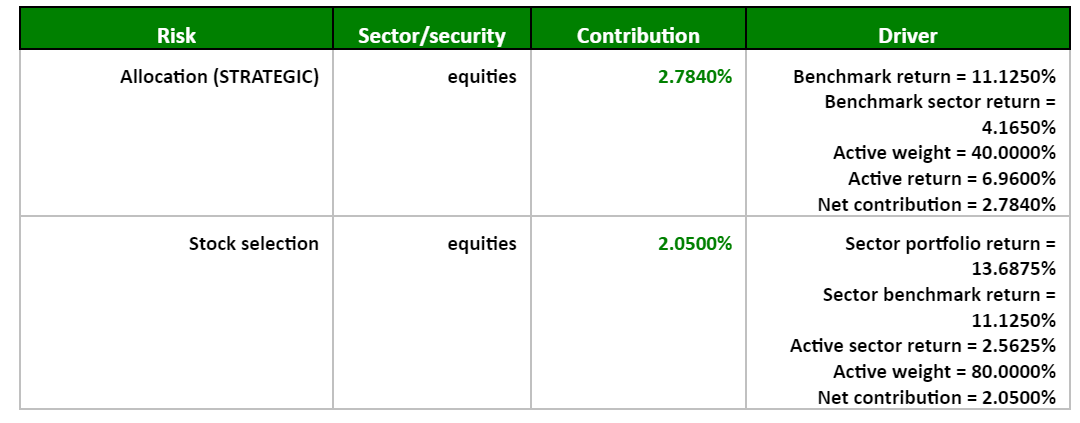

What happens when return is due to a sector decision, rather than an individual security? Let’s look at the outcome of a single-level Brinson analysis on a portfolio and benchmark holding equities, bonds and cash. The Brinson sector is ‘Strategic’.

This report shows that the highest contributor to active return was the allocation tilt taken by the equites sector. In this sector, the portfolio was 40% overweight against the benchmark, and the active return (sector return minus benchmark return) was 6.96%, which together give the net contribution shown of 2.784%.

The second highest contributor was the aggregated stock selection decisions made in the same (equity) sector. Here, the active return (portfolio sector minus benchmark sector) was 2.5625%, and the portfolio sector weight was 80%. Combined, these give the net contribution shown of 2.05%.

Configuring the context report

To generate a context report, set up an interactive report in the usual way, using the configuration settings. For instance, if you are running a Brinson analysis using the strategic variable to partition your data, set

This will tell FIA to run a Brinson report on this variable, and to generate an interactive report showing contributions at the strategic sector and security levels.

Next, add RANKED=R_A to the ReportSectors setting, with a pipe symbol separating the two set of settings:

This tells FIA to generate a standard interactive report and a context report, based on the same sector classification as used in the interactive report. The context report will have the same name as the interactive report with _TOP_BOTTOM_5_X added to the end.

The depth of the context report, which governs the number of best and worst contributions shown, is set by the RankCount variable. This has a default value of 5 but can be set to any value you wish. If you change RankCount, the number in the report’s name will also change.

Caveats

For the reader’s convenience, a ‘Net contribution’ figure is shown for each line on the context report, showing what the contribution would be, based on the numbers displayed.

However, it is important to appreciate that this contribution will often differ from the actual contribution shown in the third column of the report.

The net contribution uses a snapshot in time of the quantities shown, while the true contribution is an aggregate over time, and includes the effects of varying allocations, market conditions and positioning. In addition, smoothing can also affect contributions. So don’t expect the two numbers to always match up exactly. They do in the cases shown here, because the portfolios are small and only held over a single time interval. This will probably not be the case for a real-world portfolio, but this should not affect the use of the numbers shown, which are an indicative guide to where the numbers came from.